Makala Skinner, Research Associate, WES

[1]

[1]

While the United States has seen the number of international students from many countries fluctuate over time, Chinese student enrollment has consistently grown and driven the country’s total international enrollment. As higher numbers of students from abroad have sought a college education in the U.S., the country’s higher education financing structure has become increasingly dependent on international enrollment. Higher education institutions (HEIs) have relied more and more on the tuition of international students—increasingly Chinese students—to supplement operation budgets. Subsidizing higher education with international student tuition and fees may be running its course, however, as growth from China has decreased steadily for nearly a decade and appears to be entering a period of contraction.

Though the number of Chinese students in the U.S. has not yet decreased, continual growth is unlikely, especially in the current context, which is infused with U.S-China tensions, visa restrictions, and increased competition from other countries. The implications of this slowdown in Chinese student enrollment will reverberate throughout the higher education system as a whole as well as the broader economy writ large.1 [2] U.S. HEIs have become increasingly reliant on international students to supplement declining domestic enrollment, to meet rising administrative costs, and to buttress dwindling state funding.

This article explores the reasons why growth in Chinese student mobility is shrinking, the financial risk that this development poses to U.S. institutions, and why HEIs became reliant on international students in the first place.

Slowdown of Chinese Student Enrollment

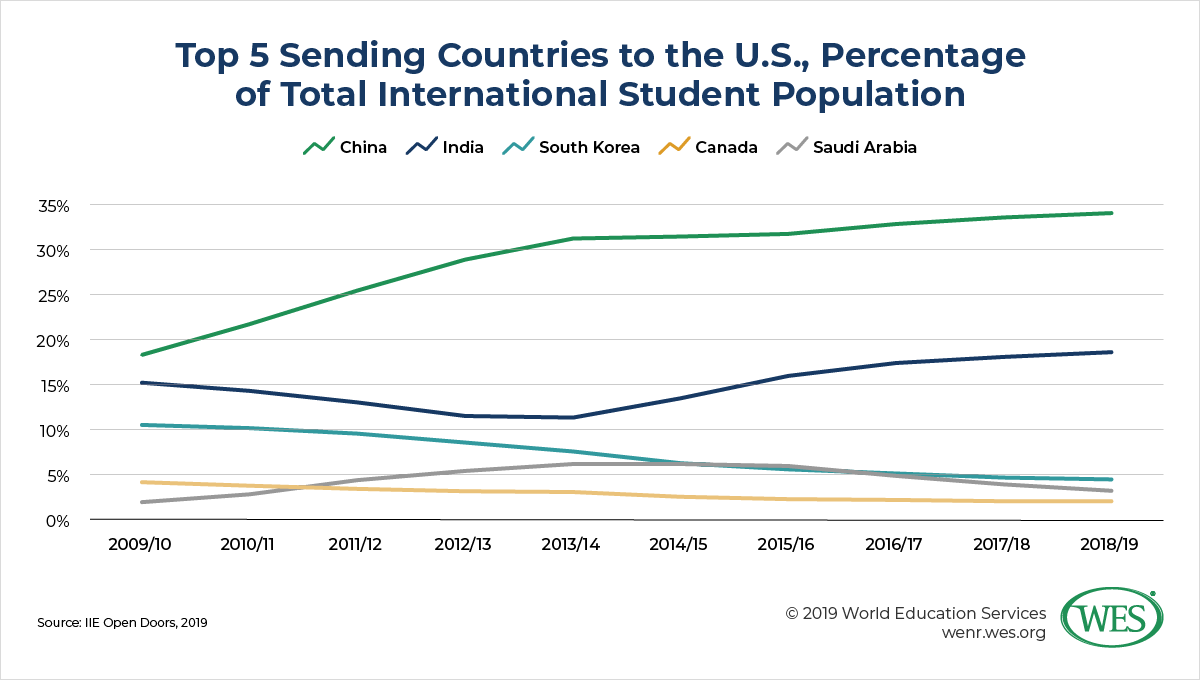

The importance of Chinese student enrollment at U.S. HEIs has grown considerably over the past decade. Chinese students have increasingly made up a larger proportion of the total international student population. For example, though Chinese and Indian students made up relatively similar proportions of the international student population in the U.S. in 2009/10 (19 percent and 15 percent, respectively), as of 2018/19, Chinese student enrollment is nearly double that of Indian student enrollment. The latest data show that Chinese students make up just over a third [3] of all students from abroad in the U.S., according to the Institute of International Education (IIE).

[4]

[4]

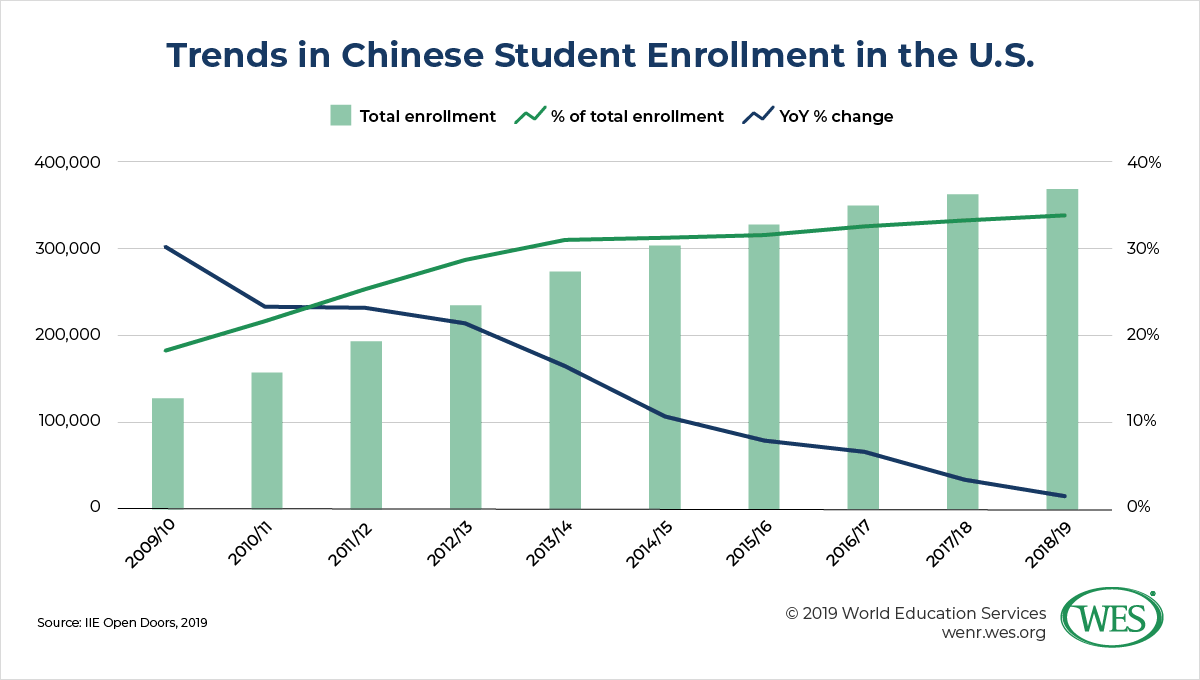

Yet even as Chinese student enrollment becomes more prominent in the U.S. each year, so too has its growth slowed down. From its year-over-year growth of 30 percent in 2009/10, Chinese student enrollment growth has consistently decreased each year and grew only 2 percent in 2018/19. This percentage shrinks further if OPT participants (who make up 19 percent of Chinese international students in the U.S.) are omitted and focus solely on enrolled students; then Chinese student enrollment grew only 0.6 percent in 2018/19 rather than 2 percent. According to IIE’s 2019 Enrollment Survey [5], the majority of participating institutions (80 percent) are somewhat or very worried about the recruitment of Chinese students. Some institutions have gone so far as to take out insurance to protect themselves from further drops in Chinese student enrollment. The University of Illinois at Urbana Champaign secured $60 million in insurance [6] coverage should there be a 20 percent decline in Chinese student tuition within one year.

[7]

[7]

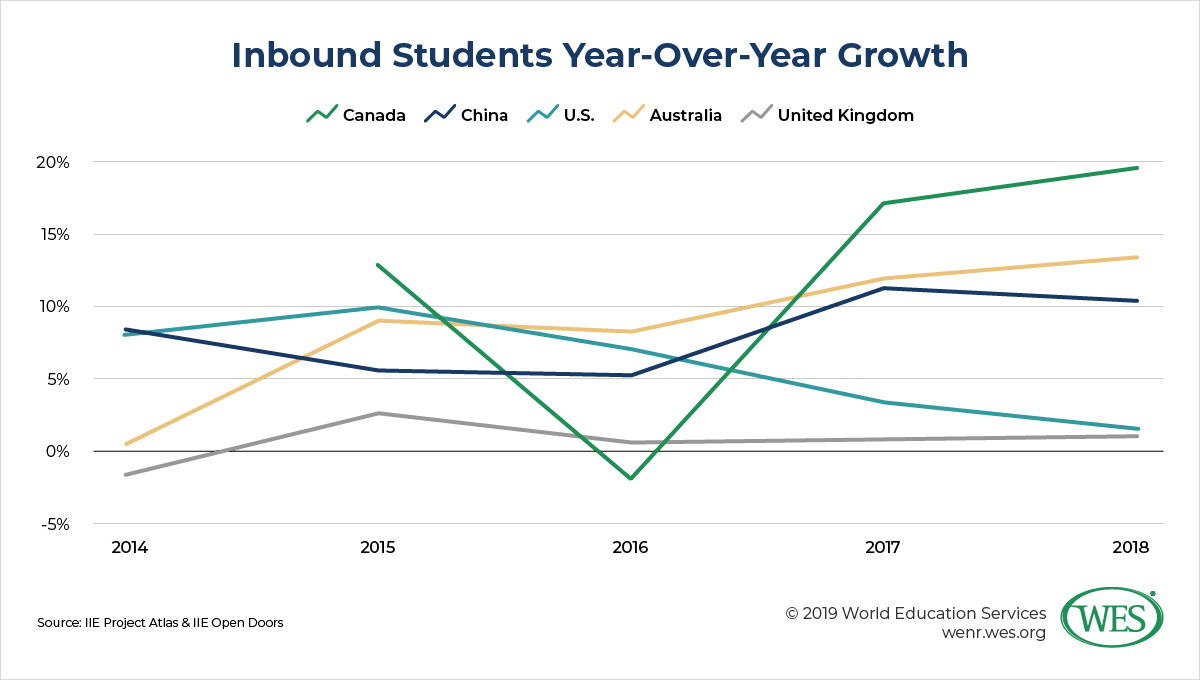

It may be tempting to suggest that the decline in Chinese student growth rates is part of a global downward trend in international student movement; however, this does not appear to be the case. In order to contrast data between countries and make an apples-to-apples comparison, this article uses IIE’s Project Atlas [8] inbound student data to examine the top five destination countries. Of the five countries that draw the most international students worldwide, year-over-year growth in the U.S. is comparatively low for 2018, according to the most recent data year available. While Canada experienced a whopping 19.8 percent increase in international students in 2018, and Australia and China saw increases of 13.5 and 10.5 percent, respectively, student flows to the U.S. increased by only 1.5 percent.2 [9] The only country in the top five to experience slower growth was the United Kingdom (1.1 percent).

And while the U.S. only saw 3.6 percent growth in total Chinese student enrollment in reporting year 2018 (and only 1.7 percent growth in the 2018/19 academic year), Australia had an 18 percent increase in Chinese students. This means that many students from China are pursuing their education abroad in countries other than the U.S., and indeed, even outside of traditional destination countries. According to Times Higher Education World University Rankings, there was a 22 percent increase [10] in the number of Chinese students going abroad between 2016 and 2018. In the U.S., however, from 2016/17 to 2018/19, Chinese student enrollment grew only 5 percent [11]. For a more detailed look at Chinese student mobility to key countries, including inbound numbers based on destination country metrics, please read our China country profile [12].

[13]

[13]

Contributors to the Enrollment Slowdown

The reasons for the slowdown of Chinese student enrollment are multi-faceted. Some are directly related to U.S. policy, while others reflect the more complex shifting of the higher education environment. Visa restrictions [14], the U.S.-China trade war [15], China’s rise [16] as a destination country, and more countries pursuing [17] international students worldwide are just a few of these reasons. Hans de Wit, director of the Center for International Higher Education at Boston College, predicts that Chinese enrollment will continue to slow. He told WES, “There’s increasing competition, there are high costs, and there is a feeling of lack of safety. There is also the whole trade war, accusations towards Chinese students, attacks on the Confucius Institutes, and warnings from the Chinese government about going to the United States.” All of these variables contribute to the deceleration of Chinese student enrollment.

In terms of policy, amidst White House concerns about intellectual property theft and national security threats, U.S. governing bodies have taken actions hindering Chinese students and academics in the U.S. In June 2018, the U.S. curtailed visas for Chinese students in some STEM [18] fields at the graduate level, changing the visa length to just one year from the previous five. This modification was introduced because of concerns that students studying certain science fields would relay technological and intellectual information to the Chinese government, and thus pose a security threat [14] to the U.S. The White House released a 36-page document in June 2018 titled: How China’s Economic Aggression Threatens the Technologies and Intellectual Property of the United States and the World [19]. The report says—under the subheading “Chinese Nationals In the U.S. as Non-Traditional Information Collectors”—that “the Chinese State has put in place programs aimed at encouraging Chinese science and engineering students ‘to master technologies that may later become critical to key military systems.’” Nearly a year later a bill [20] was introduced in Congress (in May 2019) that would preclude any person in or sponsored by the Chinese military from being granted a visa to study or conduct research in the U.S.

These visa issues have tangible consequences. In June, the Chinese Ministry of Education issued a statement [21] warning students studying in the U.S. to be aware of challenges they might encounter. The ministry cited visa delays and increased denials as adversely affecting Chinese students pursuing their degree in the U.S. More than 48 million people had viewed the hashtag associated with the alert (#教育部发布2019年第1号留学预警#, which translates to #The Ministry of Education released its first study abroad alert of 2019#) on Weibo, a Chinese social media outlet, as of mid-October 2019. Additionally, representatives at U.S. HEIs believe that visa issues are affecting enrollment. According to IIE’s 2019 Snapshot Report [5], 87 percent of participating respondents said that visa challenges are partly responsible for enrollment declines in Fall 2019; this percentage is a nearly 20 percent increase from the proportion of respondents who said visa issues contributed to enrollment declines just two years earlier in 2017. In the IIE survey [5], 83 percent of participating schools said that visa challenges are partly responsible for enrollment declines at the beginning of the 2018/19 academic year.

It isn’t only Chinese students who have come under greater scrutiny. In early 2019, the National Institutes of Health (NIH) requested information [22] from several U.S. HEIs on professors who had suspected ties to governments abroad. ScienceInsider [22] reported that “at some institutions, every researcher flagged by NIH is Chinese-American.” On top of this, U.S. HEI professors of Chinese origin have been the subject of an FBI investigation looking for individuals with ties to intelligence organizations in their home country. As a result, approximately 30 professors have had their visa revoked or put under review, according to the New York Times [23].

As these changes and investigations have been under way, the two economic giants of the world have been locked in a trade war. The U.S. and China have both imposed tariffs [24] on billions of dollars of imported goods from one another. As of October 2019, the two countries were still in negotiations [25] to try to come to trade terms that will lift the tariffs, though some progress has been made as planned tariff increases on Chinese imports were recently suspended. The trade war has bled into the higher education realm. The South China Morning Post [26] published an article in May with the title, “Trade war turning Chinese students off the US, with many opting for UK, Canada and Australia, says payments firm.” The heightened tensions between the two countries, coupled with the visa issues, have contributed to Chinese students’ turning to countries that offer more supportive enrollment pathways.

Chinese students have many countries to choose from. While previously there were just a few major destination and sending countries each, the flow of students has now become much more varied as more players have appeared on the international education stage. More and more countries are establishing internationalization strategies and setting higher education targets with the goal of attracting students from abroad. New Zealand’s International Education Strategy 2018-2030 [27], France’s A Strategy for Attracting International Students [28], the U.K.’s International Education Strategy: Global potential, global growth [29], and Australia’s National Strategy for International Education 2025 [30] are just a few of the countries taking steps to make themselves more appealing to international students. In addition, the rapid increase in programs that offer English as the language of instruction in countries like the Netherlands [31], Germany [32], and Poland [33] has made them attractive alternatives to a typically more expensive U.S. education.

Furthermore, China itself has become a prominent higher education destination. It is currently the third top destination [16] country in the world, behind only the U.S. and the U.K. This prominence is due to a variety of factors, not least of which is China’s focus on improving higher education. China’s National Plan for Medium and Long-term Education Reform and Development (2010-2020) [34] states, “By 2020, the structure of higher education shall become more balanced and distinctive, and it shall also go up a notch in talent or professional cultivation, scientific research and social service as a whole.… China’s higher education shall have vastly sharpened its global competitive edge” (Ministry of Education of the People’s Republic of China, 2010, p. 19). China’s focus on strengthening the quality of its higher education sector may be a driver for some students to pursue their education at home rather than abroad.

The Precarious Financial Position of U.S. HEIs

The lagging growth of Chinese student enrollment has consequences for the broader U.S. economy—Chinese students supplied approximate $12 billion [35] to the economy in just 2016/17—as well as for U.S. higher education as a whole. The finances and demographics of higher education have morphed over the past decade, shifting into a precarious arrangement that has universities and colleges increasingly reliant on international student tuition. Declining domestic enrollment and decreased state funding are the two primary drivers of this shift.

[36]

[36]

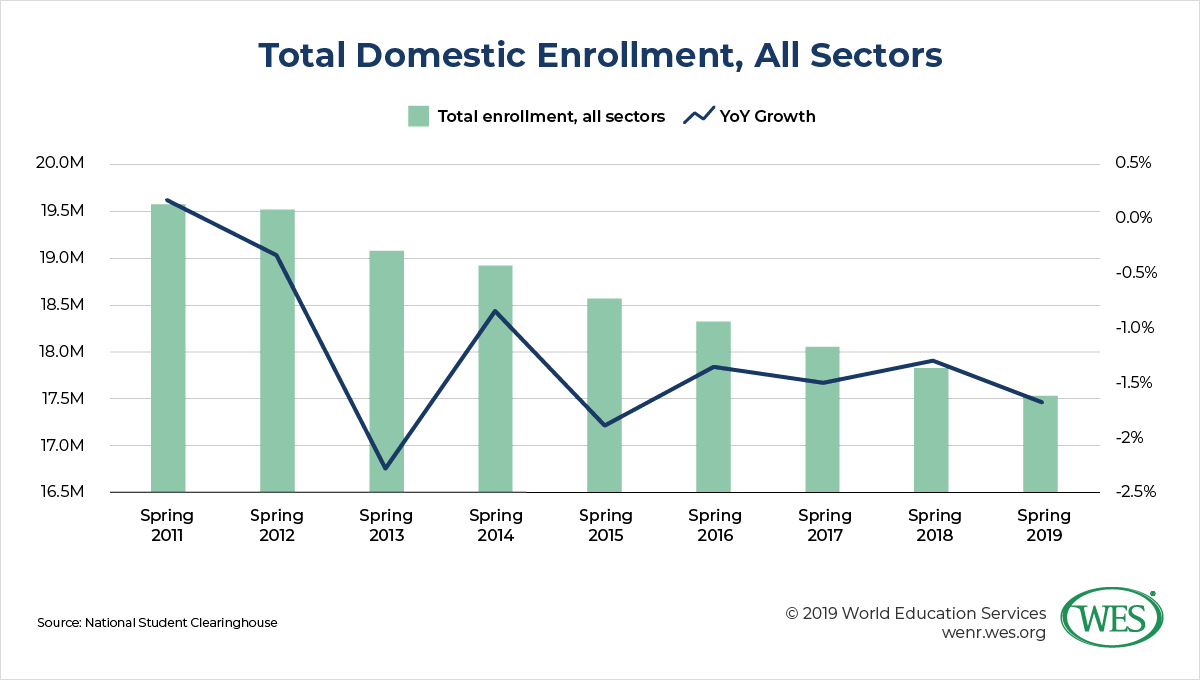

Domestic student enrollment dropped 10.3 percent from Spring 2011 to Spring 2019, according to data from the National Student Clearinghouse [37].3 [38] The overall decline is primarily driven by enrollment drops at community colleges and at for-profit, four-year institutions. When looking at four-year public institutions by themselves, there has been modest growth in enrollment over this period (2.6 percent); however, the past two years have seen successive declines. HEIs have even begun to offer in-state tuition fees to out-of-state domestic students in order to attract more students.4 [39]

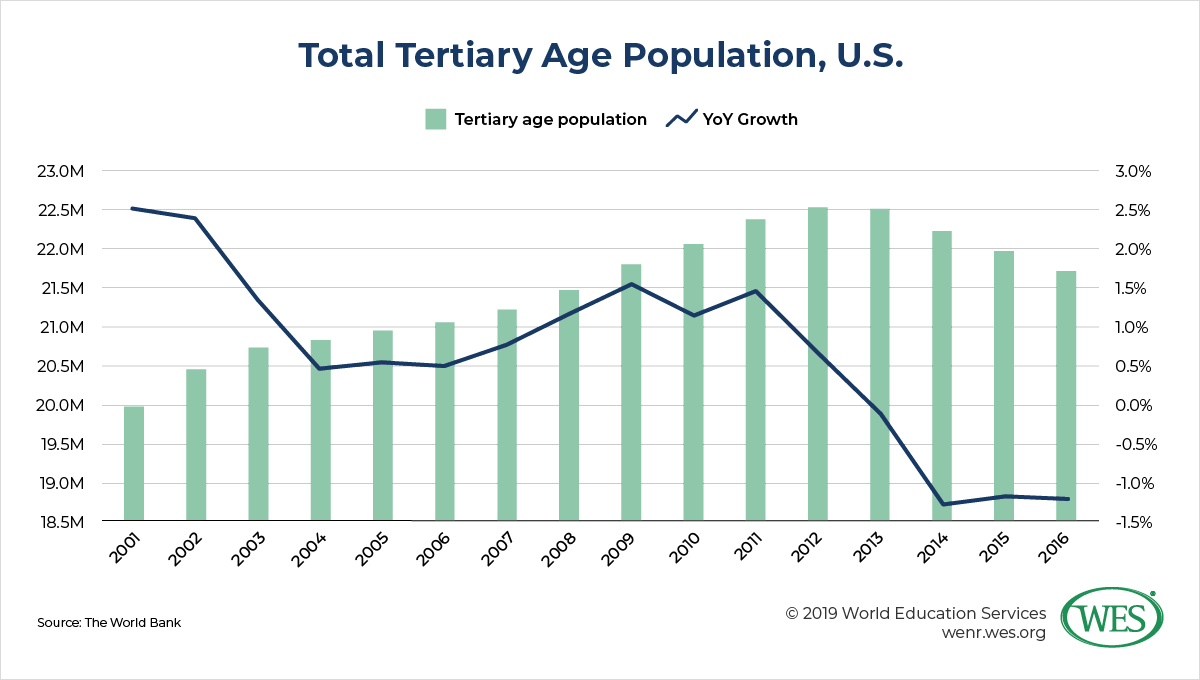

A number of factors are contributing to decreasing domestic enrollments. The U.S. unemployment rate [40]—3.6 percent—is the lowest it has been since 1969. The relatively robust job market drives [41] many people to go straight into the workforce rather than pursue higher education. In conjunction with the economy, the college-age population in the U.S. plateaued in 2012 and declined from 2013 to 2016.5 [42] This decline will likely continue since the number of births [43] in the U.S. has trended downward for the past several decades, according to the National Center for Health Statistics.

The rising cost of higher education in the U.S. is also contributing to enrollment declines, as students and their families become unable to afford tuition. The average in-state cost [44] of a public four-year institution increased by 24 percent from 2009/10 to 2019/20. The average in-state tuition is currently6 [45] $10,440 for a public, four-year institution, and $36,880 for a private, four-year school. The cost of pursuing a degree is rising more rapidly than income; Forbes reported in 2018 [46] that college costs increased at eight times the rate that employment income did. The high cost of education outstrips the ability of many families to pay, and likely contributes to the decline in domestic student enrollment.

[47]

[47]

In tandem with this, the government has made significant cuts to funding for public HEIs since the mid-aughts. In 2017, government support for public institutions was approximately $9 billion less than it was a decade earlier, according to the Center on Budget and Policy Priorities [48]. The sharp decreases in state funding were a consequence of the Great Recession. The 2008 financial crisis impacted not only state funding but also HEI endowments, which often help pay operating costs. Harvard University [49], for example, lost 22 percent of its endowment—or $8 billion—because of the financial crisis.

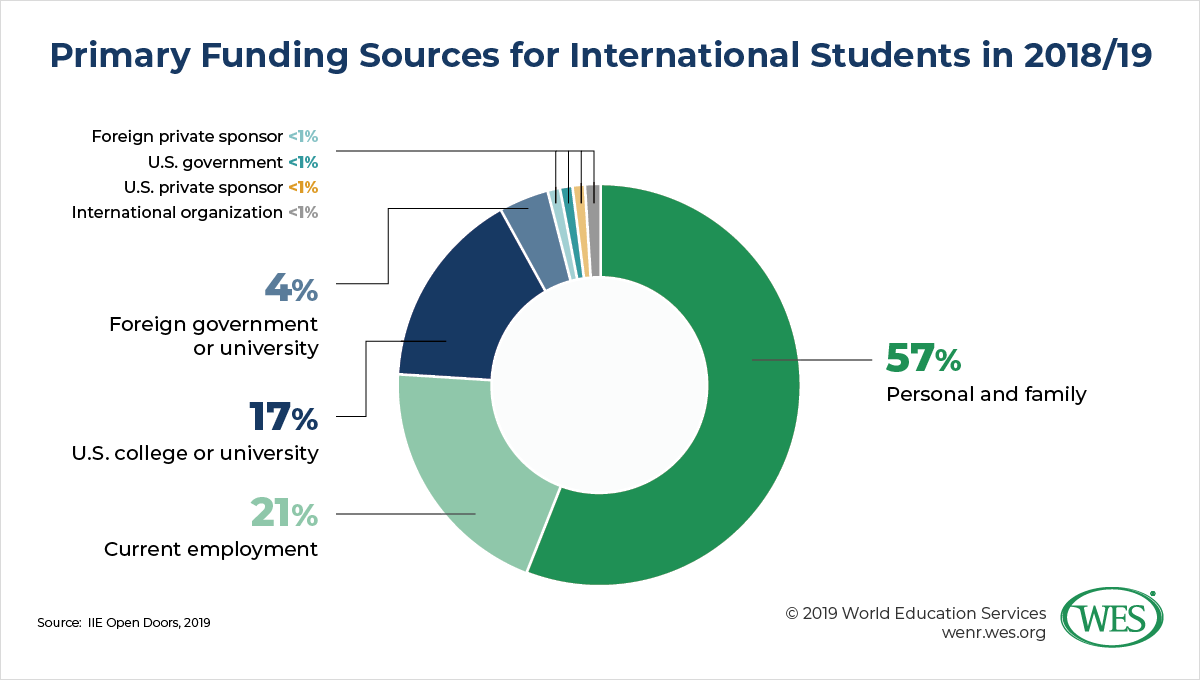

Dual decreases in these financial streams (domestic students plus state funding) has left HEIs searching for ways to make up for lost revenues, which helps account for the skyrocketing costs of higher education in the U.S. International students have become a crucial tool for institutions as HEIs strive to balance budgets. Students from abroad pay out-of-state tuition; the average cost of a four-year out-of-state degree at a public institution was a staggering $26,820 [44] in 2019/20. Importantly, more than half [50] of international students fund their education with personal and family resources, paying the full tuition amount. In fact, only 17 percent of international students funded their education with resources from their institution (such as scholarships, grants, and assistantships) in 2018/19, according to IIE.

Yet, as reported by the PIE News [51], Allan Goodman, CEO of IIE, said, “Everywhere I travel talking with parents and students, the number one concern they have is about cost. American higher education is expensive—more expensive than other countries.” In a 2019 WES survey, 32 percent of Chinese students attending U.S. HEIs said that tuition was more than they expected it would be, and 53 percent said that books were more expensive as well.

[52]

[52]

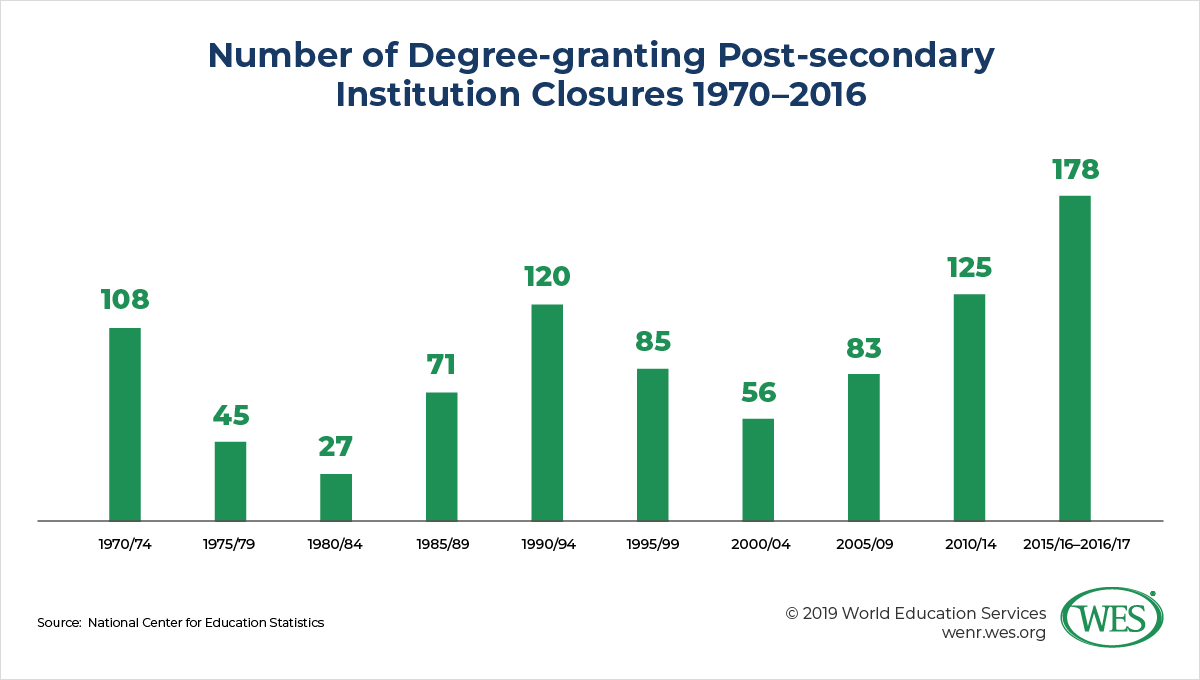

The U.S. HEI financing structure is already proving unsustainable in light of unprecedented school closures. According to the Chronicle of Higher Education [53], between 2014 and 2018, 11 public, 129 private non-profit, and a whopping 1,094 for-profit institutions7 [54] closed their doors. Some of these institutions have closed down altogether, while others have been absorbed by other institutions. The National Center for Education Statistics [55], which tracks closures of solely degree-granting institutions, shows that institutional closures are not a new phenomenon; however, they do appear to be becoming more pronounced. The graphic below charts the number of degree-granting post-secondary institution closures over five-year periods from 1970 to 2016.8 [56] From 1970 to 1974, 108 schools closed their doors; a similar spike in closures occurred between 1990 and 1994. However, over just a two-year period, from 2015/16 to 2016/17, more institutions closed than at any other five-year period in the previous 46 years. This pattern reveals a distinct trend of colleges and universities in the U.S. ceasing operations. In addition to the reasons listed above, it is worth noting that administrative costs [57] have risen significantly over the past several years as well; these rising costs also likely contribute to budgeting shortfalls.

[58]

[58]

Conclusion

The current strategy of using international student enrollment—along with over relying on Chinese student enrollment specifically—is an ineffectual short-term solution for U.S. HEIs, one that is already starting to unravel. A third of international students are from China, and Chinese enrollment growth has consistently slowed over the past several years. Depending on enrollment from just one country puts institutions at the mercy of socio-political tensions outside of their control.

Schools should consider taking measures to ensure their financial health. Hans de Wit noted that the consequences of decelerating Chinese student enrollment will not affect all HEIs in the same way. Public and state universities and smaller colleges are likely to be most affected. De Wit advises, “Diversify your international student population, and don’t make your budget dependent on international students. It is such a vulnerable situation to be in, certainly in the current global and political climate. See [international students] as an added value from a quality point of view, but do not make them the driver of your economic future.”

In addition to diversifying their international student populations, HEIs can enhance institutional service offerings to help mitigate declines in international student numbers—since positive student experiences are associated with retention as well as word-of-mouth referrals. Recent WES research [59] on the international student experience shows that while international students are overwhelmingly satisfied with their experience studying in the U.S. (91 percent), there are several areas where institutions can better support students as well. Regarding Chinese students specifically, research findings show several areas that may be helpful for HEIs to provide more supportive programming or initiatives. Here are just a few examples:

- Only 56 percent of Chinese students feel that they have a strong social network at their school.

- Fifty percent of Chinese students find it difficult to form close friendships with domestic students (which is 9 percent more than the average for all international students).

- Chinese students are 11 percent less likely than Indian students to find the U.S. a welcoming country.

- Chinese students are the most likely to experience discrimination at their institution because of their nationality (40 percent).

The report offers actionable recommendations for institutions to address these challenges and provide exceptional support to international students in the U.S.

Given U.S. HEIs’ precarious financial landscape, especially in light of international student declines and a slowing of Chinese enrollment specifically, it is important for schools to take an earnest look at their budgets and funding streams. It will be helpful for institutions to identify where they may be putting themselves at risk financially, how international students fit within that equation, and what they can do to correct course.

1. [60] International students in the U.S. supplied $45 billion [61] to the economy in 2018 alone.

2. [62] The most recent U.S. data year available through Project Atlas is 2017, which corresponds with IIE’s Open Doors data for academic year 2016/17. To maintain consistency, we used IIE’s Open Doors data for academic year 2017/18 for the 2018 U.S. data included in the graph.

3. [63] Total enrollment includes students enrolled at 4-Year Public, 4-Year Private Nonprofit, 4-Year For-Profit, and 2-Year Public.

4. [64] Source: Interview with Hans de Wit, director of the Center for International Higher Education at Boston College

5. [65] 2016 is the latest available data year the World Bank provides.

6. [66] 2019/20 academic year

7. [67] For-profit institutions include large-scale institutions such as ITT Technical Institute in Indianapolis, which enrolled 10,070 students at the time of its closure, and very small specialty schools such as Harmon’s Beauty School, which had a roster of six. For more information, you can reference the Chronicle of Higher Education’s searchable database here [68].

8. [69] 2016 is the most recent data year available.